The Late Wire Change Is Where the File Goes Dark

Last-minute wire instruction changes create ambiguity, pressure, and stale assumptions. What an escrow file should record when payment details change close to funding.

Every escrow officer knows the email. Subject line: "Updated wire instructions." Timestamp: uncomfortably close to funding. Tone: breezy. "Please use the attached going forward — the other account is having issues. Thanks so much!"

Most of the time it is real. Sellers change banks. Payoff lenders reissue demands. Attorneys redirect proceeds. That is what makes the late change such a reliable vehicle: it borrows the shape of a routine event.

In INTERPOL's Operation First Light 2026 casework, the single largest intercepted transfer — USD 6.6 million, stopped through the agency's stop-payment channel — was a business email compromise against a Singapore commodity firm, run by criminals posing as a supplier. Strip the industry labels and it is the move an escrow office sees weekly.

A known counterparty. A plausible reason. New payment coordinates. And a clock.

Everyone says late changes are risky. The useful question is why, mechanically, the file goes dark at that exact moment. Three failures converge.

Why escrow should care

The late change concentrates escrow's entire fraud exposure into its least-documented event. It arrives when the file feels finished, when attention has moved to the next closing, and when the person best positioned to catch it is busiest.

And if it goes wrong, the late change is the first thing everyone examines. The bank's recall paperwork, the carrier's questions, the examiner's timeline — all of it orbits the moment the payment details moved.

An office that treated the change as a routine attachment has a gap at the point of highest scrutiny. An office that treated it as an event — logged, re-checked, decided — has its strongest page exactly where it needs one.

Ambiguity: which instruction governs?

A change creates two versions of the truth, and files are bad at versions.

The original instructions live in the opening package. The new ones live in Tuesday's email. A middle version might exist in a phone note. Unless the office marks succession — this supersedes that, as of this time, per this request — the file holds contradictions, and the answer to "which instruction governs" lives in the officer's head.

Our guide on conflicting instructions covers the disputed version of this problem. The fraud version is worse, because both "versions" claim to be from the same party, and only one is.

Pressure: the re-check feels like friction

A change early in the file gets the full treatment. The same change at 4:40 the day before funding meets a different office — one where re-confirming feels like reopening settled business and delaying real people.

The request usually arrives carrying its own justification: "the other account is frozen, and we can't miss Friday." That line supplies both the reason to act and the reason not to check. Fraudulent changes are timed late because lateness converts the re-check into an imposition.

None of this describes a weak officer. It describes a normal one, at the moment the file was designed to find.

There is a staffing angle too. Late changes tend to arrive when the usual officer is out — the Friday before a long weekend, the week someone covers a colleague's desk. A covering officer knows the file least, trusts the paperwork most, and is likeliest to treat "updated instructions attached" as an administrative item. If your office has a rule about instruction changes, the coverage desk needs it most.

Staleness: the confirmations quietly expired

This one does the most damage. The office confirmed the seller's account in week one — by callback, properly. A change in week six does not just add information. It silently cancels that old confirmation while leaving it in the file, looking like coverage.

The officer's memory says "this file was confirmed." True — of a state of the world that no longer exists.

Meanwhile, sounding like a legitimate counterparty on a quick confirming call keeps getting easier. As we wrote in our piece on GPT-Live, fluid natural voice is now ordinary software behavior, which makes "I called the number in the new email and it sounded like her" weaker than it has ever been.

The confirmation that counts is the one performed after the change, through a source that predates it.

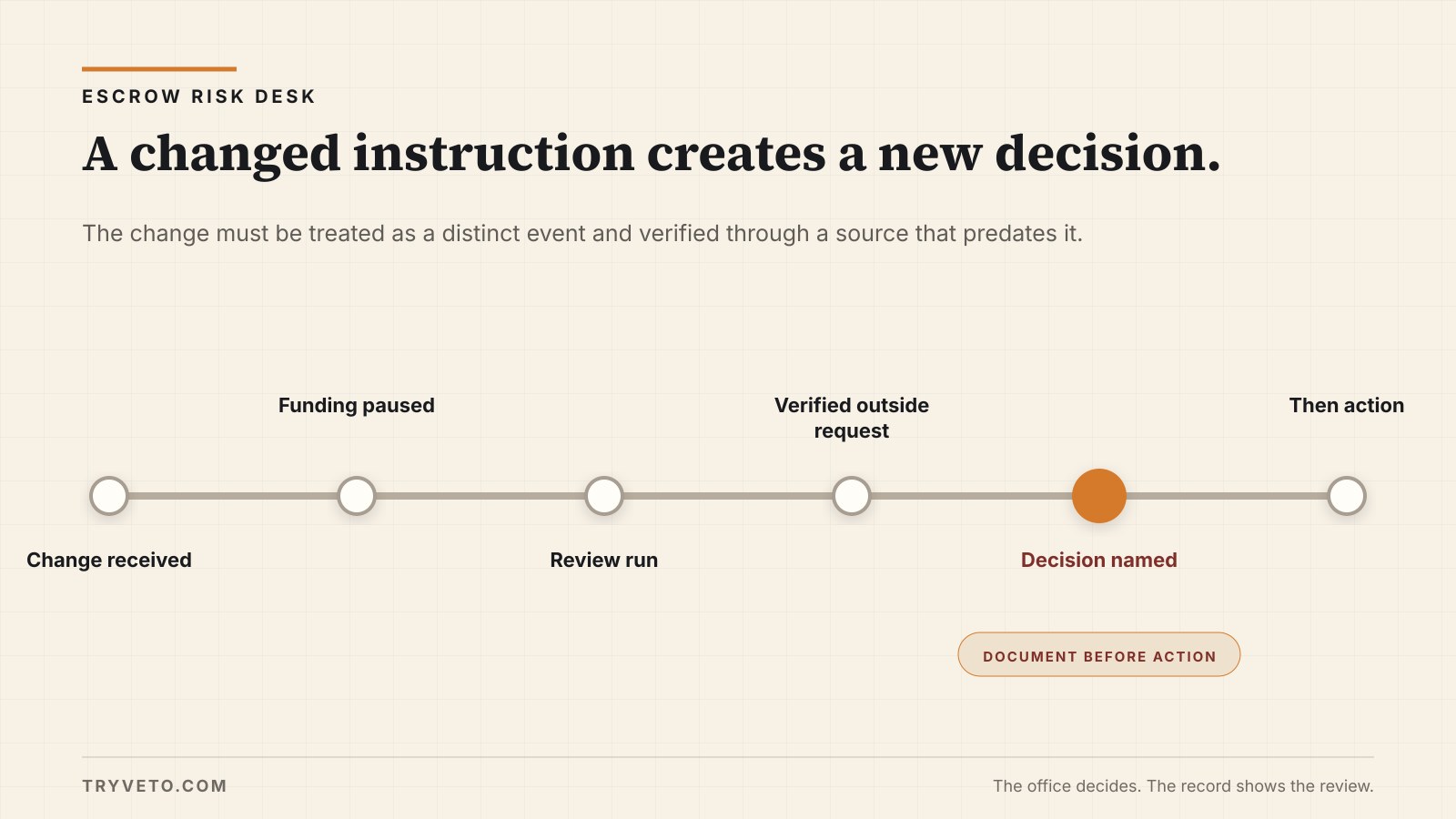

What should be written down before money moves

Before the money moves, the file should answer five questions:

- What changed.

- What was checked, and against which source.

- What stayed open.

- Who reviewed.

- What the office did.

For a late change, each question gets a sharper edge. What changed means old value to new value — bank, account, beneficiary — with the request preserved, timestamped, and the stated reason in the requester's words. What was checked means contact through a source row that predates the change, the person reached, the facts confirmed — plus an explicit line that prior confirmations of the superseded instructions no longer apply. What stayed open is retained in plain words. And the decision carries names: the reviewer, the accepter if anything stayed open, and the office's action — proceed on the new instructions, revert to the old, or hold pending an owner exception.

One page. It doubles as the succession record that answers "which instruction governs" forever after.

Operator takeaway

Treat every late change as two things at once: a probably routine event, and the most examined moment your file will ever contain if it is not.

The move that covers both is the same. Re-check through a channel older than the change, mark the succession, and put a name on the decision.

The change email took the sender thirty seconds.

Give the record ten minutes.

— Sebastian Heyneman

Sources

- Over 5,800 arrests, USD 293 million intercepted in global fraud bust (INTERPOL, July 9, 2026)

- Introducing GPT-Live (OpenAI, July 8, 2026)

- Related on this blog: What to Do When Buyers and Sellers Give You Conflicting Instructions

Boundaries: the USD 6.6 million case is as reported by INTERPOL and involved a commodity firm, not an escrow office; the escrow mapping is ours. The staffing observation about coverage desks is field experience, not a dataset.

See a sample Review Record.

One page showing what changed, what was checked, what stayed open, and who reviewed it.