The Pre-Disbursement Review: What Has to Be True Before Money Leaves Trust

Funding day. Three files closing, two opening, and the proceeds instruction on the largest file came in by email six weeks ago.

Funding day. Three files closing, two opening, and the proceeds instruction on the largest file came in by email six weeks ago.

Escrow losses don't usually happen because nobody was paying attention. They happen at final funding, under deadline, when the file "felt closed" and one instruction in it was stale, unverified, or changed at the last minute. The wire goes out clean against a dirty instruction, and everything after that is recovery, claims, and reconstruction.

The fix isn't more caution in general. It's one short, specific review between "we're ready to fund" and "the wire is released," with evidence in the file that it happened. Here's that review.

Who this guide is for

Independent California escrow offices where officers release their own disbursements, or where a manager approves wires informally, "looks good, send it." Especially resale shops where funding days stack up and the same officer is closing three files while opening two.

What this guide helps you do

- Define what "verified" actually means for each outbound wire.

- Catch stale and superseded instructions before funding, not after.

- Separate the hands that prepare from the eyes that release, even in a two-person office.

- Handle legitimate exceptions without blocking the closing or waving the risk through.

- Leave a record showing who reviewed what, when, and what the office decided.

1. Seller proceeds: match the payee to the file, not the email

The proceeds wire is the largest and most targeted disbursement in most files, and the instruction usually arrives by email or portal, sometimes weeks before funding. The classic failures: the account belongs to a fraudster who got into the seller's email; a real late change never made it into the file; or the payee name doesn't match the vested seller and nobody reconciled it.

Check: the payee matches the party entitled to proceeds under the instructions. The account was verified by callback to a number sourced independently of the instruction email, from the opening package, a prior verified call, the listing agent's known contact. Never the signature block of the email that delivered the instruction. And the instruction in hand is the most recent one in the file.

Record: the instruction used (date and source) and the callback: date, time, number called, where that number came from, who answered, what was confirmed, officer's initials.

Don't assume an instruction verified at opening is still good at funding. And an inbound call verifies nothing, you don't know who dialed.

2. Payoff wires: the demand is an instruction too

Payoff demands feel institutional, so they get less scrutiny than proceeds. Fraudsters know it, altered demands are a standing pattern. A demand arrives by email with the right letterhead and a substituted account. A legitimate demand expires and you fund stale figures. A junior lienholder's demand comes from a servicer nobody validates.

Check: the demand came through a channel you can trust, lender portal, or confirmed by calling the lender at a number from its own website or the borrower's statement, never the demand document. Account and reference numbers match prior demands if any exist. The demand is unexpired, with per-diem run to the actual funding date.

Record: the demand version funded, how the channel was verified, the expiration and per-diem math.

Don't assume plausible figures plus the right logo equals authentic. And don't assume a re-issued demand kept the same account.

3. Stale instructions: age is a risk factor

The longer the gap between collecting an instruction and funding it, the more room for a change, legitimate or not, to have happened without reaching the file. The seller switched banks. The loan got sold. An amendment sits unfiled in someone's inbox, and funding proceeds on the version everyone remembers instead of the version that governs.

Check: at the pre-disbursement review, confirm the effective date of each instruction and search for anything later, emails, amendments, portal messages, that supersedes it. Then set a house rule: any wire instruction older than your threshold gets re-confirmed before funding. Thirty days is common. Pick yours and write it down.

Record: the date of the instruction used, confirmation that nothing later exists, and any re-confirmation performed.

Don't assume the newest email is filed. Search; don't rely on memory.

4. Callback evidence: a callback that isn't documented didn't happen

Most offices "always call to verify." Far fewer can show it, and when a claim hits, the difference between those two offices is enormous. The failure isn't skipping the call, it's the note that says "verified per phone" and nothing else, which can't distinguish a real verification from a call to the fraudster's number printed on the fake instruction.

Check: every callback note answers five questions. What number. Where the number came from. When. Who answered. What exactly was confirmed, bank name, last four, payee name, amount range.

Record: that structured note. One line with those five facts beats a paragraph without them.

Don't assume calling the number on the wire instruction counts. The source of the number is the whole point.

5. Second review: separate the hands that prepare from the eyes that release

On a busy day in a small office, the preparer, reviewer, and releaser are often the same person, which collapses the one control that catches both fraud and honest error. A transposed digit or a superseded instruction sails through because the person who built the wire is the person who checked it.

Check: before release, someone other than the preparer confirms: payee matches file, account matches the verified instruction, amount ties to the settlement statement, no unresolved exception. In a two-person office, the second set of eyes is the owner. In a solo office, the control is a forced time gap plus a written self-review against the checklist, weaker, but real, and worth naming as your policy instead of pretending otherwise.

Record: reviewer name, date and time, what was compared, and the approval.

Don't assume a signature means the reviewer re-verified anything. The record should show what was actually compared.

6. Exceptions: name them, don't bury them

Real closings produce legitimate exceptions, the payoff portal is down, the seller is reachable only at a new number, the lender funds an hour before cutoff. Offices tend to either block (and blow the closing) or wave through (and eat the risk). The right move is usually to proceed with a named, owned exception, the danger is handling it verbally, where everyone remembers it differently and a reasonable decision looks like negligence in hindsight.

Check: what exactly couldn't be completed, what compensating step was taken, who accepted the open item, and what the follow-up is.

Record: an exception note, the open item, the compensating check, the approver, the decision, the date. "Held pending owner exception" is a legitimate file status when it's a documented office decision.

Don't assume a verbal owner OK covers the officer. If the owner accepted the risk, the file should say so in the owner's name.

7. Funding-day pressure: the highest-risk hour of the file

Fraudulent changes cluster at final funding because that's when the pressure to release is highest and the appetite for one more phone call is lowest. Agents call. Lenders call. Everyone wants the wire out by cutoff, and the step that gets skipped is exactly the one that would have caught the problem.

Check: nothing new. The same review, protected from compression. The house rule that matters: a wire that misses today's cutoff goes tomorrow; a wire to the wrong account may never come back.

Record: if you're pressured to skip a step, record the pressure and the decision. "Agent requested immediate release; review completed in full before release at [time]" is a sentence that protects everyone.

Don't assume urgency correlates with legitimacy. It correlates with the opposite.

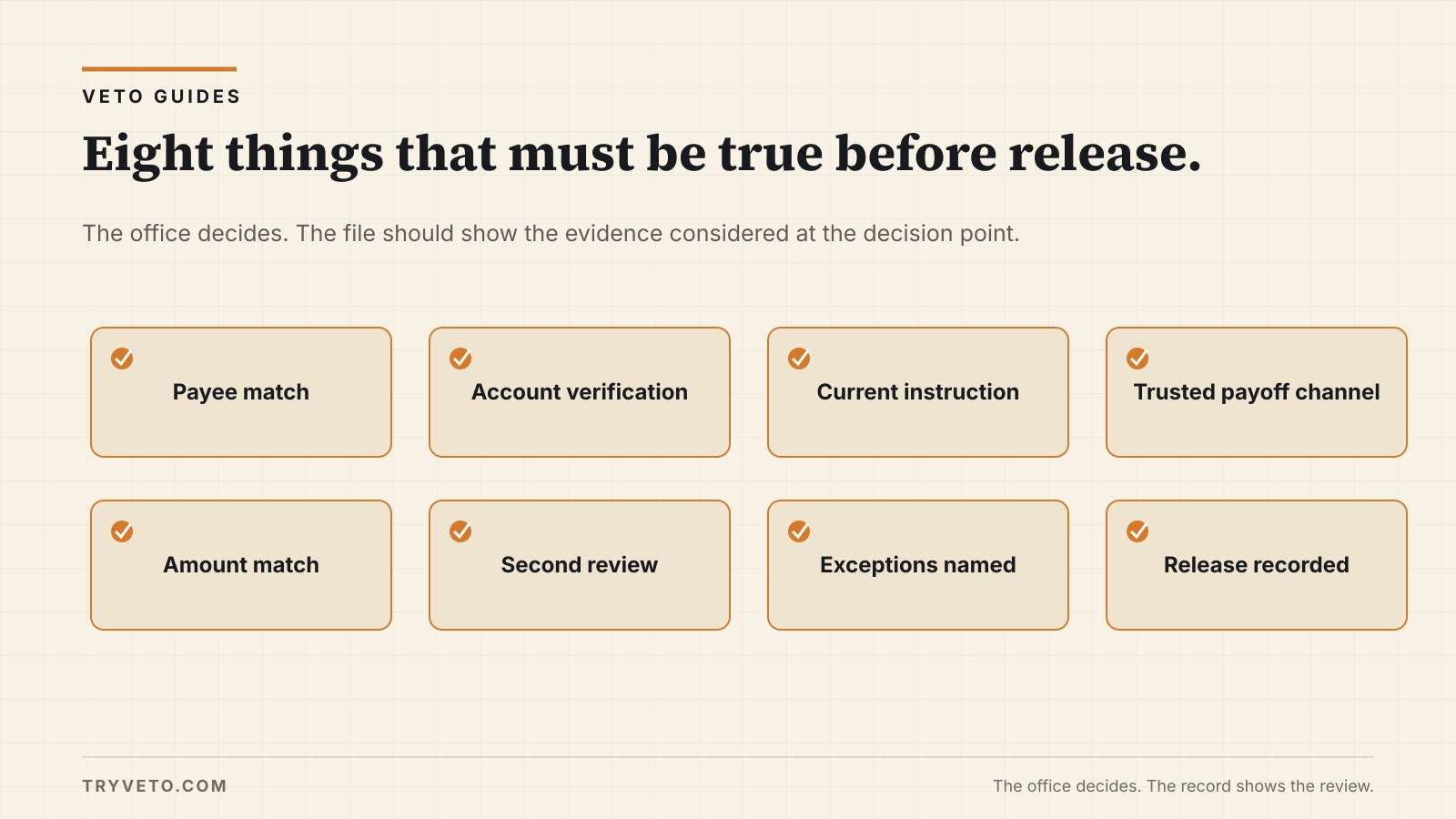

Pre-disbursement checklist table

| Step | What must be true | Evidence in file |

|---|---|---|

| Payee match | Payee = party entitled under instructions | Instruction + statement cross-check |

| Account verification | Callback to independently sourced number done | Structured callback note |

| Instruction currency | Latest version in hand; stale ones re-confirmed | Date check; re-confirmation note |

| Payoff channel | Demand obtained via trusted channel | Demand version + channel note |

| Amount match | Wire ties to settlement statement | Reviewer comparison note |

| Second review | Non-preparer reviewed and approved | Reviewer name, time, items compared |

| Exceptions | Open items named and owner-approved | Exception note |

| Release | Wire released per approved instruction | Release confirmation |

Risk / what to check / what to record

| Risk | What to check | What to record |

|---|---|---|

| Spoofed seller instruction | Callback to independent number; payee match | Callback note with number source |

| Altered payoff demand | Channel of receipt; account continuity | Demand version, channel verification |

| Stale instruction funded | Effective date vs. threshold; later versions | Currency check; re-confirmation |

| Preparer error | Second-person comparison before release | Reviewer approval, items compared |

| Pressure-driven skip | Every step ran despite deadline | Pressure/decision note |

| Buried exception | Open item named and owner-accepted | Exception note with approver |

Callback script, seller proceeds

"Hi, this is [name] at [office] on your escrow, file [number]. For your protection I verify wire instructions by phone. I'm going to read you the bank name and the last four digits of the account we have, please confirm they're yours. I won't ask you to read me a full account number, and we never accept changes to these instructions by email alone. [Confirm bank, last four, payee, approximate amount.] Thank you, I'm noting this call in your file."

Exception note template

Exception, File [number] Open item: ____ (e.g., payoff portal down; demand confirmed by phone to number from borrower's statement) Compensating step: ____ Open item retained: Y / N, follow-up: ____ Reviewed by: ____ Approved by (owner/manager): ____ Date/time: ____ Decision: proceed / hold. Status: held pending owner exception / released.

Common mistakes

- "Verified per phone" with no number, no source, no name, a note that proves nothing.

- Reserving scrutiny for seller proceeds and waving payoff demands through because they look institutional.

- Letting the preparer approve their own wire because the reviewer was at lunch.

- Re-confirming a changed instruction by replying to the email that changed it.

- Documenting only the files that felt risky, so clean files carry no evidence of review at all.

What to save in the file

Before release: the governing instruction with date and source; the structured callback note; the payoff demand version and its channel verification; the settlement statement tie-out; the reviewer's approval showing what was compared; any exception note in the approver's name; the release approval. After funding: the bank's outgoing wire confirmation. Seven items. If every funded file has them, you can reconstruct any wire in five minutes, for a client question, a bank inquiry, or a claim.

When to escalate

Owner or manager before release whenever an instruction changed within days of funding, a callback can't reach an independently sourced number, a demand's channel can't be validated, or anyone pressures you to skip a step. Your bank immediately if a wire may have gone to a wrong account, recall odds decay by the hour. Carrier notice per your policy terms, and counsel before statements to parties about fault. Your policy and counsel govern; this isn't legal advice.

How Veto fits

This whole guide reduces to one page in the file: what changed, what was checked and against which source, what stayed open, who reviewed, what the office did. That's what Veto records, the instruction's source row, what matched, the open item retained, the reviewer, and the office's action.

You still decide and release. The record shows the review came before the money.

Printable checklist

PRE-DISBURSEMENT REVIEW, FILE #____ Date: ____ Officer: ____

[ ] Governing instruction identified, date: ____ source: ____

[ ] No later instruction/amendment in file or inbox

[ ] Instruction within age threshold (or re-confirmed: ____)

[ ] Payee matches entitled party per instructions

[ ] Callback done, number: ____ source of number: ____

[ ] Confirmed: bank / last four / payee / amount range

[ ] Payoff demand version: ____ channel verified: ____

[ ] Demand unexpired; per-diem to actual funding date

[ ] Wire amount ties to settlement statement

[ ] Second review by non-preparer: ____ time: ____

[ ] Exceptions: none / noted and owner-approved (attached)

[ ] Release approved by: ____ Released: ____

[ ] Bank wire confirmation saved to fileOne page in the file before money moves.

Your office decides. Veto records what was reviewed, what stayed open, and who reviewed it.