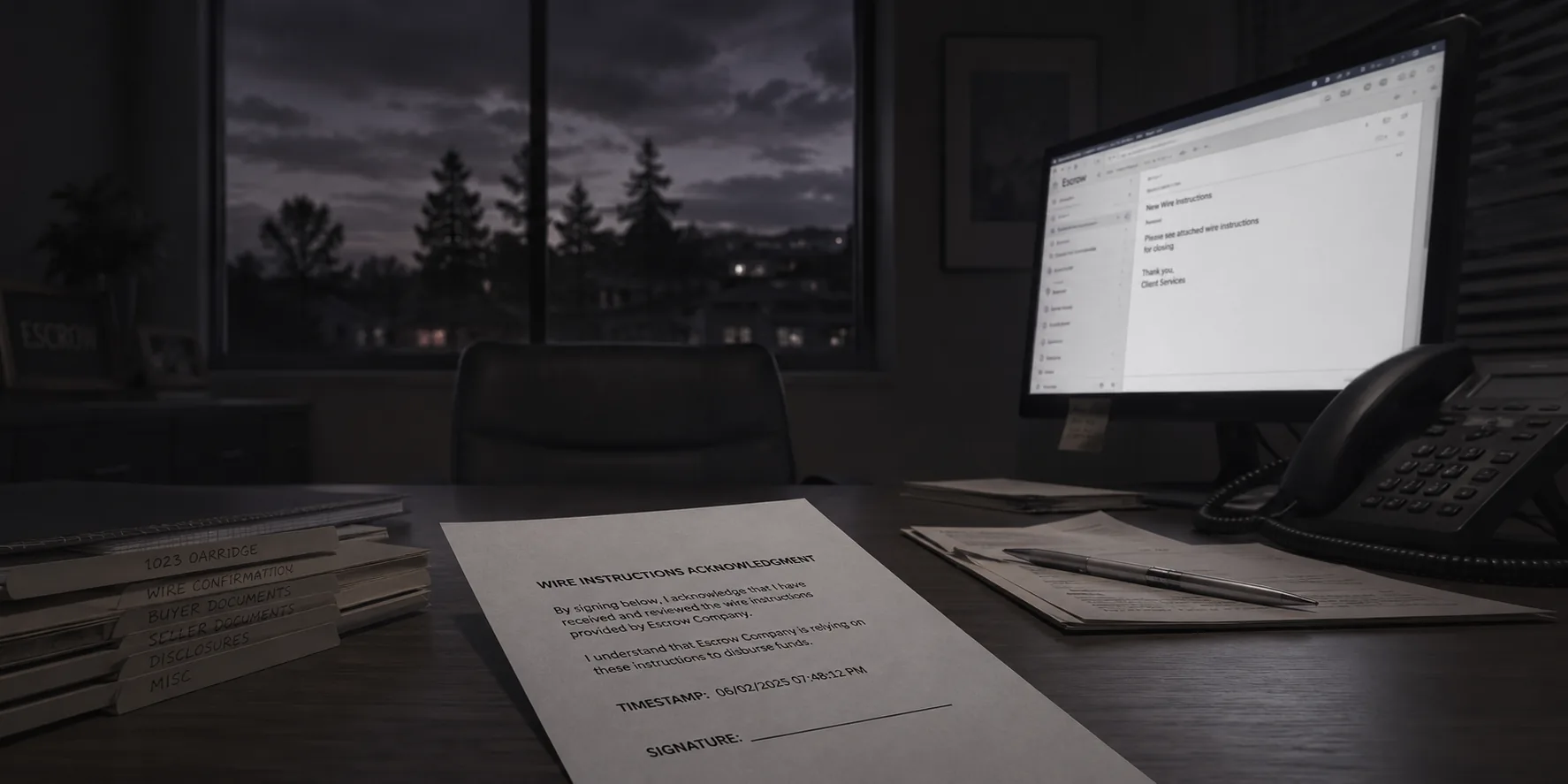

On April 9, 2026, an escrow company in Anaheim received an email. It came from a law firm claiming to represent a creditor, and it demanded $26.5 million from an open escrow file. The file's instructions were explicit: no funds before closing, and no disbursement on email instructions alone.

The company wired the $26.5 million the same day.

Six days later it wrote to the law firm asking for the money back. The money did not come back. In June, the Commissioner of Financial Protection and Innovation took possession of Centerstone Escrow, appointed a conservator, and put a number on the damage: a trust shortage of at least $31,870,208.34, which the Department tied to about $57 million in unauthorized disbursements.

It reads like a wire-fraud story. It isn't one, not exactly. The wire is only the final event. What the Department's findings actually describe is what was missing in the hours before it: an instruction gets read, a demand gets matched against it, someone in the office reviews and decides. At Centerstone, on April 9, no documented authorization or review record appears in the Department's findings. The order says so in the sentence the Department keeps writing, in case after case:

There were no escrow instructions or authorizations to support this disbursement.

The 2026 docket rhymes

Across the recent Escrow Law docket, the cases are different. The control failure keeps rhyming. From the Department's filed documents:

- **Axiom Escrow Inc.** Possession on May 15, after a whistleblower complaint. Trust funds moved between escrow files that shared no parties: $100,000 here, $242,000 there, $850,000 in a single wire, nine transfers in one series, with newer deposits covering older shortages. Estimated shortage: $299,154.72.

- **Superstar Escrow, Inc.** Ordered out of the business on March 20. It had asked to surrender its license with 30 escrows still open, four carrying debit balances totaling $76,078.96, and roughly 70 outstanding checks totaling $108,306.40 against a trust account that might not cover them. The office disclosed one shortage. The Department's review found three more.

- **Melrose Escrow, Inc.** License revoked on April 20. No dramatic wire. It tried to surrender, and the closing audit came due in January. It never arrived, and neither did the annual audit, the financials, or the records.

- **Jerry Ward.** Barred from escrow employment, management, or control. Thirty-two unauthorized checks from various escrow files over thirteen months, to payees who were not parties to the escrows. The examples in the order are almost modest: $3,810 in property-tax refunds, a $3,459 leftover balance, $1,697 a borrower had returned to escrow. The total was $90,237.52. Nobody reviewed the small checks, so there were many of them.

- **Beverly Jane Stickler.** Barred from escrow employment, management, or control. The Department found she kept a fake escrow file, attached to no transaction, and fed it with the quiet money real closings leave behind: a $68,181 tax holdback, a $24,225 tax holdback, a $7,121 refund a buyer never saw. From it she wrote checks to herself totaling $270,688.73. All of it: $545,464.20.

- **Lisa Elaine McGuire.** Accused of issuing a closing statement showing $316,253.27 in buyer deposits when substantially less had actually arrived, and of 37 unauthorized disbursements across fifteen files, a $73,438.85 shortage. She settled with the Department in June.

The same question, seven times

These are not the same case. A criminal demand letter, an officer stealing small, a manager stealing large, one file's funds covering another's hole, an office that simply could not produce its records when asked. But hold them together and the Department is asking every office the same operational question.

Before the office acted, where was the review?

Not the closing file. Not the email chain. Not the bank reconciliation months later. The review, and the record it left. A record that answers five plain questions:

- What instruction or condition triggered the action?

- What did the office check?

- What was still open?

- Who reviewed it?

- What did the office decide?

Escrow is full of moments where the answer isn't obvious in real time. Funds arrive late. Instructions change. A payoff looks off. A demand letter arrives sounding like a law firm. Everyone wants the file closed. The job is not to remove judgment from those moments. Escrow is judgment. The job is to make the judgment visible.

What the examiner actually asks

The test in these orders is unglamorous. For each disbursement: produce the instruction that authorized it, and show the review that matched the money to it before it moved.

The dollar amount barely matters. Ward's bar was built on checks smaller than most escrow fees. Centerstone's collapse ran to eight figures. The finding was identical.

And notice what the software in this industry stores. Documents, and every one of these offices had documents. Task lists. Closing packages. Useful, all of it. But the failure mode in these orders is not that there was no folder. It is that money moved, or a file closed, without a durable record of the decision that made the action defensible.

The record is the defense

A defensible office can show, for every money movement: we checked these items, these were still open, this person reviewed it, the office chose this action, here is the receipt, with a name and a timestamp on it.

That doesn't make an office perfect. It does something more realistic. For owners, it's supervision they can actually see. For staff, it's protection: proof they did the review, not just a memory of it. For an examiner, it's the answer to the only question these orders ever ask.

Escrow trust is built file by file. This year's docket shows it is lost the same way, file by file, in the quiet moment when someone decides the money can move. That moment needs a record.

The offices in these orders would have given a great deal, in hindsight, to be able to produce one. The offices still standing can build it now.

Veto exists for that moment: the office decides; Veto records what was checked, what stayed open, who reviewed, and what action the office took.

Sources and boundaries

Sources: DFPI Actions and Orders, Escrow Law docket, 2025 to 2026. Notice and Summary of Findings re Centerstone Escrow, Inc. (June 11, 2026); Notice and Summary of Findings re Axiom Escrow Inc. (May 15, 2026); Order to Discontinue re Superstar Escrow, Inc. (March 20, 2026); Accusation to Revoke re Melrose Escrow, Inc. (March 9, 2026, revoked April 20, 2026); Order Barring Jerry Ward (March 23, 2026); Order Barring Beverly Jane Stickler (December 15, 2025); Accusation re Lisa Elaine McGuire (November 13, 2025, settled June 8, 2026). Figures are from the Department's filed documents. Accusations are allegations; bars and possessions reflect the Commissioner's findings and orders. The docket is public at the California DFPI Escrow Law page.