The review receipt standard

What the Veto Record is, what it contains, and what it does not do.

When wire instructions change — new account, new payee, different bank, different amount — the escrow office faces a decision. Release, hold, or reject.

The Veto Record exists to capture that decision and the evidence that informed it. It is a file-ready record of disbursement review before high-risk funds move. Built from operator conversations and the self-audit in Can your file prove the disbursement review?.

The review timeline. Instructions arrive. The operator reviews them. The office decides. Someone signs off. Funds move or do not. The record captures everything between arrival and office action — the part most production systems were not designed to hold.

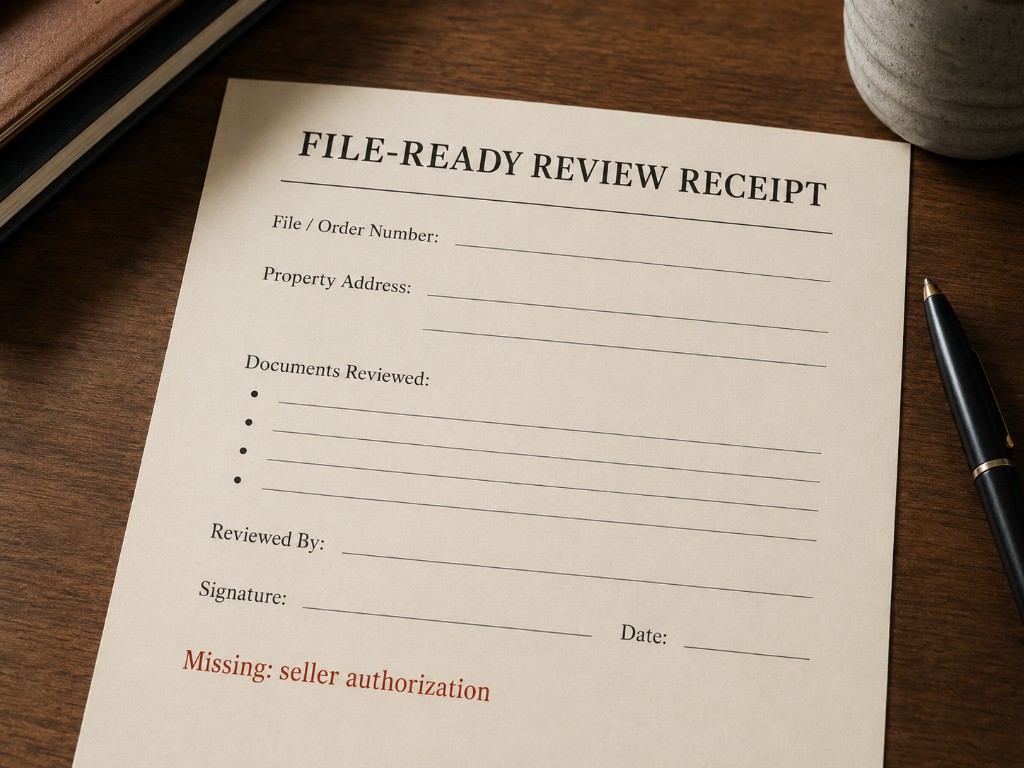

What the record contains.

What changed. The specific instruction that differs — not "proceeds changed" but "destination account changed from Chase •••• 4521 to Wells Fargo •••• 7803."

What was retained. Prior notes, documents, and communications that bear on the change — including prior callbacks and authorizations.

What was checked. Each check with its result and its limitation stated. Routing confirmed active does not prove account ownership. Payee match via API is not live bank confirmation. The record says so.

What stayed open. Missing authorization, unanswered callback, domain mismatch not run, document referenced but never received. Stated, not hidden.

Who reviewed it. Named reviewer and when the review was saved.

What the office did. Hold, release, escalate, return, or proceed with a documented exception.

What it is not. It is not an approval. The office decides. The record records.

It is not a guarantee. No record prevents fraud. The record shows the work was done.

It is not a substitute for judgment. The record captures reasoning — it does not replace it.

Veto records the review. It does not approve, authorize, guarantee, insure, verify, release funds, validate identities, confirm bank accounts, authenticate payees, or make wires safe to send. The escrow office remains the release authority.

The standard is simple: if it informed the decision, it belongs on the record. If it did not, it does not.

Read the full standard on /standard. Or start one Veto Record on a closed or redacted file and answer the judgment question yourself.

Would it be unreasonable to try this on one closed or redacted disbursement file?

Start one Veto Record →Or try a sample with fictional data.