File Completeness: Documentation That Holds Up When Someone Else Reads Your Files

Every escrow file gets read twice. Once by your office, while the transaction is live, with all the phone calls, hallway conversations, and officer memory attached.

Every escrow file gets read twice. Once by your office, while the transaction is live, with all the phone calls, hallway conversations, and officer memory attached. And once, if anything ever goes wrong, by a second reader: an examiner, an auditor, a claims adjuster, opposing counsel, or the successor officer picking up a colleague's desk. The second reader has no context, no memory, and every incentive to find the gap.

This guide is about building files for the second reader, documentation habits, trust-account support, exception handling, and evidence of review, maintained as routine instead of assembled under pressure.

One note on scope: California independent escrow companies are licensed and examined by DFPI. Per DFPI guidance, licensees submit audited financial statements within 105 days after fiscal year-end, file the Report of Escrow Liability by February 15, report new officers, directors, and employees within 10 days, and sit for examination every two to four years. This guide covers operational habits, not legal requirements.

Who this guide is for

Owners and managers of DFPI-licensed independent escrow companies, and the officers and processors who build the files, especially offices where documentation varies by desk, "it's in the email somewhere" is a common answer, and exam or audit prep means a scramble.

What this guide helps you do

- Define "complete" so completeness is checkable instead of debatable.

- Keep trust-account records that tie to files without archaeology.

- Turn exceptions from verbal folklore into documented office decisions.

- Purge staleness, superseded instructions, expired demands, orphaned records.

- Make evidence of review a byproduct of daily work, not a special project.

1. Define "complete", or you can't audit it

Most offices believe their files are complete. Ask three officers what complete means and you'll get three answers. Each private standard produces files that vary by desk, and the gap only surfaces when a second reader compares files and asks why one has callback notes and another doesn't.

Check: whether you have a written file-content standard, the documents, instructions, verifications, approvals, and closing records every file type must contain, by stage. One page per file type is plenty.

Record: the standard itself, versioned and dated, plus an initialed completeness check at defined stages, funding and closing are the natural two.

Don't assume the software's folder structure is a standard. Empty folders organize nothing.

2. Instructions: the governing version, identifiable at a glance

Files accumulate instruction versions, originals, amendments, corrections, changes. The file has to make obvious which version governed each action. Otherwise a second reader finds two conflicting instructions and no indication which one you funded against, and even a correct decision now looks like a coin flip.

Check: amendments are filed with dates and supersession noted; the pre-disbursement record names the governing instruction by date and source; rejected or unverified changes are retained and marked, not discarded.

Record: every version received, including the rejected ones, each labeled: governing, superseded, rejected, unverified.

Don't assume deleting a fraudulent or mistaken instruction "cleans" the file. The rejected instruction plus the review that rejected it is some of the strongest evidence a file can hold.

3. Trust-account support: every entry ties to a file

The trust account is the center of an independent's regulatory life, and reconciliation is necessary but not sufficient. The three-way can balance while an individual disbursement lacks its instruction, demand, or approval in the file, and balanced totals with unsupported entries is exactly the pattern a second reader drills into.

Check: each month, pull a sample of entries and ask of each: does the file contain the instruction authorizing this disbursement, the verification, the approval, and the bank confirmation? And do aged items, dormant balances, uncashed checks, small residuals, carry current status notes instead of silence? (Unclaimed funds run on legal timelines, California's dormancy table lists escrow accounts at three years, and holders run owner due diligence, file the annual Notice Report, and remit on the state's schedule.)

Record: reconciliations with reviewer sign-off, the monthly sample tie-out, and a status note on every aged item.

Don't assume reconciliation performed equals reconciliation reviewed. The record should show who reviewed it and when.

4. Exceptions: the decision belongs in the file, in someone's name

Real files produce judgment calls that deviate from your own standard, a document accepted in nonstandard form, a disbursement on the owner's say-so, a step deferred. In most offices these live in memory. A year later, the deviation looks like an oversight because nothing marks it as a decision: the officer remembers the owner's approval; the file shows a skipped step.

Check: every departure from your standard generates a short exception note, what the standard called for, what was done instead, why, who approved, what open item was retained.

Record: that note, in the approver's name, filed at the time of the decision. "Held pending owner exception" as a documented office status is a decision. The same facts undocumented are a gap.

Don't assume exceptions read as weakness. A file with named, reasoned exceptions reads as a controlled operation. Silent deviations read as an uncontrolled one.

5. Stale records: the file should tell the truth about now

Files rot in place, expired demands, abandoned contact numbers, old estimated statements, instructions superseded by events. Each stale item is a chance for a later action, or a later reader, to rely on something no longer true: a funding run on expired figures, a callback to a number the seller left behind, a stale document taken as your operative understanding.

Check: at each stage gate, opening complete, docs out, funding, closing, run a quick currency pass. Are the operative documents current, and are the superseded ones marked?

Record: supersession notes ("Demand dated __ superseded by demand dated __") and the stage-gate check itself.

Don't assume filing order communicates status. Second readers don't read chronologically. Markings travel with the document; order doesn't.

6. Evidence of review: unrecorded reviews didn't happen, to the second reader

Offices review constantly, wires, statements, documents, and record almost none of it. The work is real; the evidence is absent. Then, in an exam or a claim, the office has to argue "we always check that," which persuades no one, instead of pointing at a record.

Check: each key review leaves a minimum artifact, who reviewed, what was compared, when, and the outcome (clean, or exception noted). One structured line per review. Essays won't be sustained and aren't needed.

Record: review entries at the control points that matter most: instruction verification, pre-disbursement, reconciliation review, closing completeness.

Don't assume more words mean better evidence. A minimal record completed every time beats an elaborate one completed sporadically. And documenting only the files that felt risky teaches the second reader that your routine files weren't reviewed.

7. Ownership and cadence: habits need a name and a date

All of the above fails as a one-time cleanup. It works only as cadence with named owners, otherwise the standard is written, the templates exist, and six months later usage has drifted back to the officers who liked it anyway.

Check: monthly, the owner or manager does the reconciliation review and the sample tie-out. Per file, the officer runs the stage gates. Quarterly, pull three random closed files and read them cold, as the second reader, no explanations allowed.

Record: the quarterly cold-read note: what the files showed, what was missing, what changed as a result.

Don't assume the cold read will be comfortable. Its value is exactly the discomfort, captured while it's cheap.

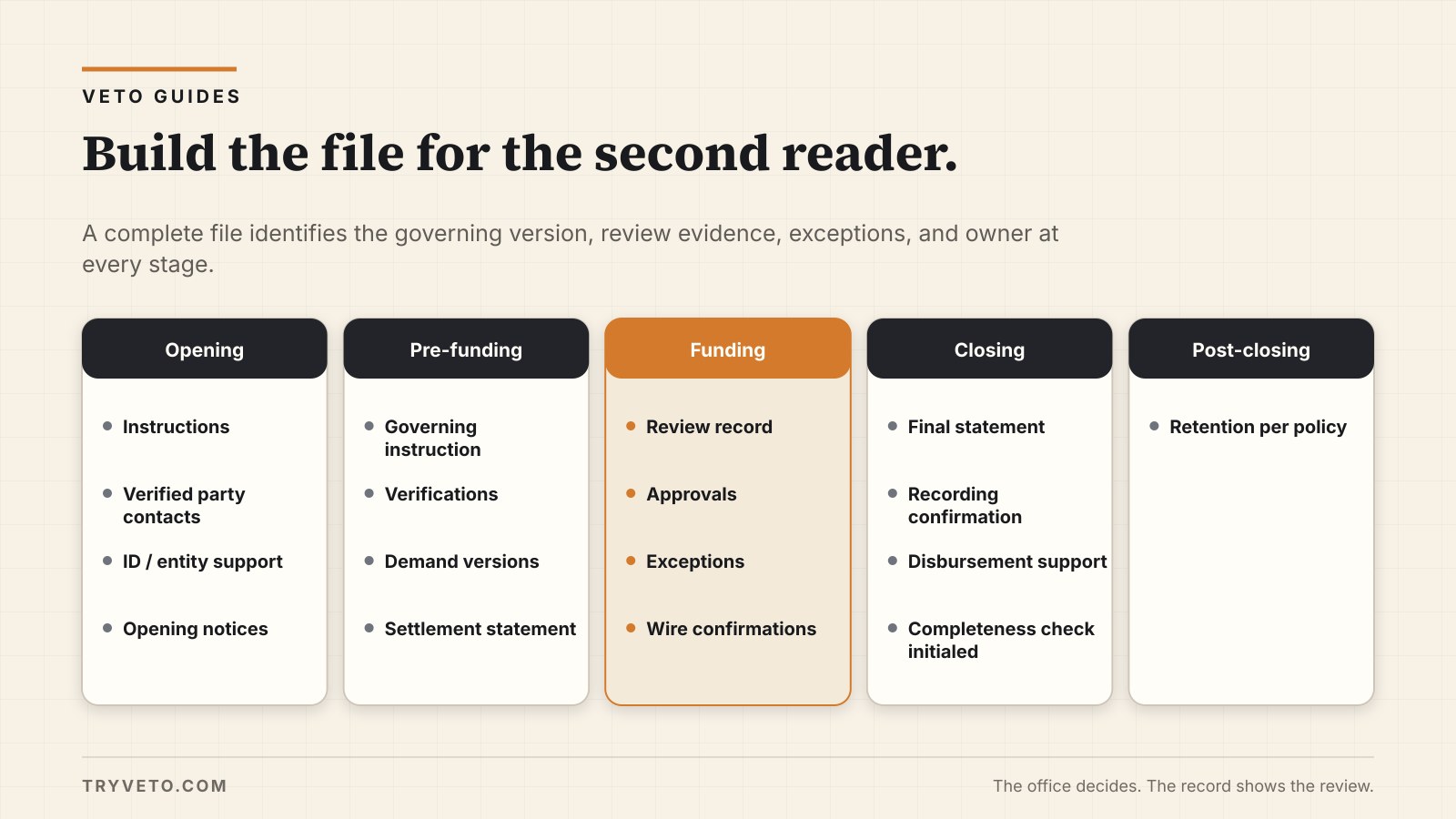

File completeness checklist table

| Stage | Must be in the file | Checked by |

|---|---|---|

| Opening | Instructions; verified party contacts; ID/entity support; opening notices | Officer |

| Pre-funding | Governing instruction named; verifications; demand versions; settlement statement | Officer + reviewer |

| Funding | Pre-disbursement review record; approvals; exceptions; wire confirmations | Reviewer |

| Closing | Final statement; recording confirmation; disbursement support; completeness check initialed | Officer |

| Post-closing | Retention, at least five years from close of escrow per DFPI guidance | Owner/manager |

Risk / what to check / what to record

| Risk | What to check | What to record |

|---|---|---|

| Ambiguous governing instruction | Version labels; supersession notes | Status on every instruction version |

| Unsupported trust entry | Monthly sample tie-out, entry → file | Tie-out note, reviewer initials |

| Silent deviation | Exception notes on every departure | Note in the approver's name |

| Stale document relied on | Stage-gate currency pass | Supersession notes; gate initials |

| Invisible diligence | Artifact at each control point | Who / compared what / when / outcome |

| Habit decay | Quarterly cold read of closed files | Findings and changes made |

Internal review note template

Review Note, File [number] Type: instruction verification / pre-disbursement / reconciliation / closing completeness Reviewed by: ____ Date/time: ____ Compared: ____ against ____ Result: clean / exception noted (see note dated ____) Open item retained: none / ____

Owner approval note template

Owner Approval, File [number] Matter: ____ Standard procedure: ____ Action approved instead: ____ Basis: ____ (fact vs. judgment noted) Open item retained: ____ Follow-up owner: ____ by ____ Approved by: ____ (owner/manager) Date/time: ____

Common mistakes

- Writing a beautiful procedures manual and never building the one-page per-file standard officers actually check against.

- Reconciling faithfully while never sampling whether entries have file support.

- Discarding rejected instructions and failed drafts, destroying the evidence of your own vigilance.

- Documenting heavily on scary files and leaving routine files bare.

- Treating exam prep as an event. Offices that document as they go don't prepare, they print.

What to save in the file

Every instruction version with a status label. Verification records including the source of every phone number used. Demand versions with supersession notes. The pre-disbursement review record. Every exception and owner-approval note. Reconciliation reviews touching the file's funds. Wire and recording confirmations. The initialed completeness checks at funding and closing. DFPI guidance sets retention at a minimum of five years from close of escrow, with "close" read broadly, final disbursement or the last transaction activity, and electronic records must stay accessible, downloadable, printable, and in compliant non-erasable form. The operating rule is simpler: if the office relied on it, decided with it, or deviated because of it, it stays in the file.

When to escalate

Owner or manager when a completeness check can't be satisfied before funding, a trust entry lacks file support, an exception exceeds the officer's authority, or a cold read reveals a pattern rather than a one-off. Your CPA or auditor on reconciliation anomalies. Carrier notice per policy terms when a documentation gap connects to a potential loss. Counsel before responding in writing to any regulator inquiry beyond routine correspondence. For DFPI exam or reporting questions, current DFPI guidance and counsel govern, not this guide.

How Veto fits

Everything above amounts to one discipline: reviews leave records. Veto makes that discipline cheap, each review captures what changed, what was checked and against which source, what stayed open, who reviewed, what the office did, in the moment instead of in retrospect.

The office keeps deciding exactly as it does today. The file simply shows it.

Printable checklist

FILE COMPLETENESS & REVIEW EVIDENCE, MONTHLY Month: ____

Per file (at funding and closing):

[ ] Governing instruction labeled; superseded versions marked

[ ] All verifications include the source of the number used

[ ] Pre-disbursement review record present

[ ] Exceptions documented in the approver's name

[ ] Stage-gate completeness check initialed

Monthly (owner/manager):

[ ] Three-way reconciliation completed AND reviewed (sign-off)

[ ] Trust-entry sample tied to file support (count: ____)

[ ] Aged/stale items carry current status notes

[ ] Exception log reviewed for patterns

Quarterly:

[ ] Cold read: 3 random closed files, no explanations

[ ] Findings recorded: ____

[ ] Standard/template updated if needed (version: ____)

Annually:

[ ] File-content standard reviewed and re-dated

[ ] Retention practices checked against the five-year DFPI minimumOne page in the file before money moves.

Your office decides. Veto records what was reviewed, what stayed open, and who reviewed it.