Singapore Is Building Anti-Scam Infrastructure. Escrow Is Still Running on Callbacks.

Singapore's Anti-Scam Centre and five banks foiled 600+ scam attempts before funds moved. What national scam infrastructure teaches a California escrow office about the pre-release review.

On July 7, the Singapore Police Force announced that its Anti-Scam Centre and five banks had disrupted more than 600 scam attempts in two months.

The operation ran May 1 through June 30, with DBS, UOB, OCBC, Standard Chartered, and GXS. Police and banks exchanged signals fast enough to send over 3,800 alerts to more than 3,300 customers while the scams were still running. More than $38 million in losses never happened.

The key word in the release is not "arrested." It is "averted."

The money never left.

Why escrow should care

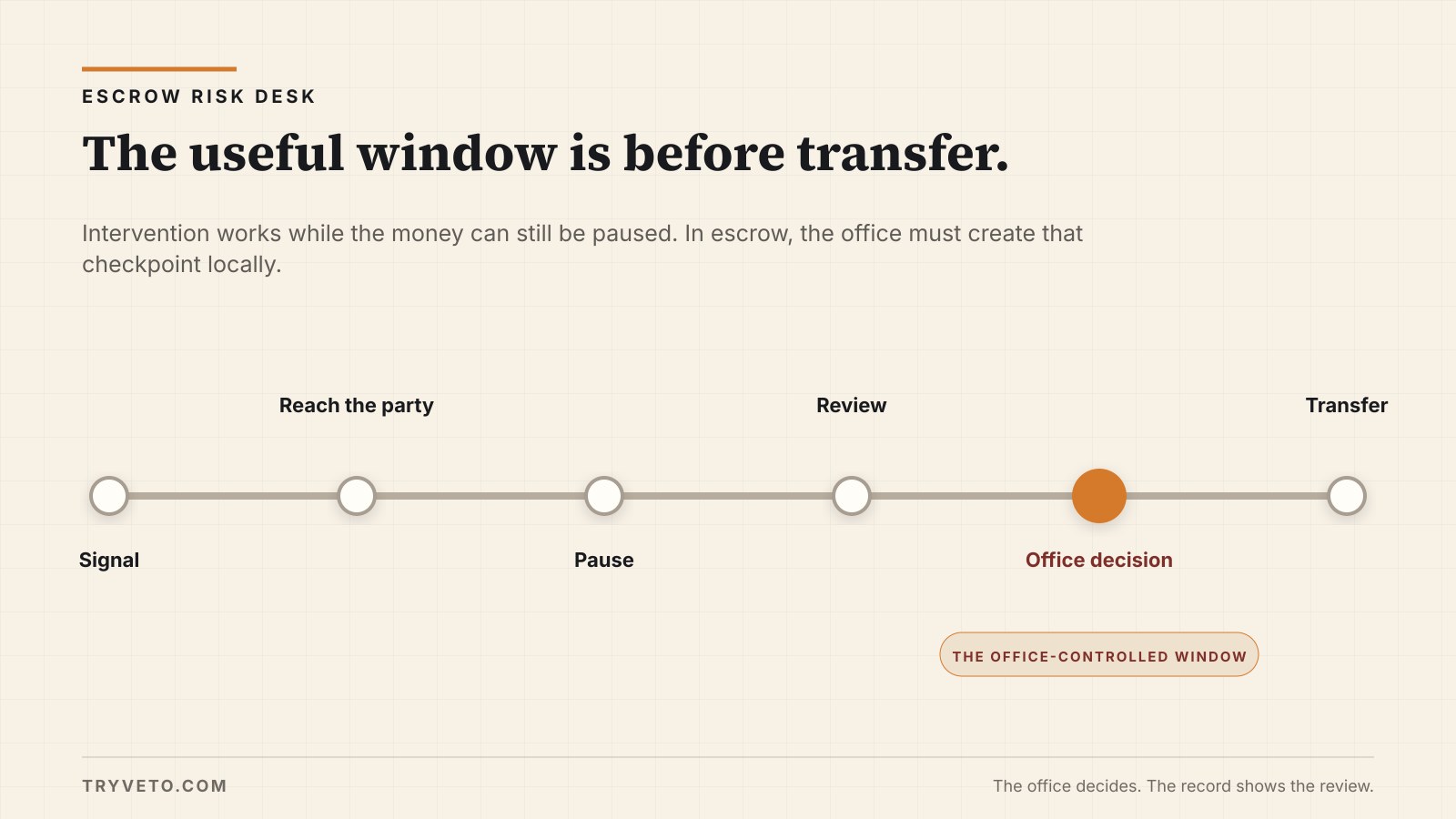

Escrow sits on the exact pattern these systems exist to intercept: large transfers, hard deadlines, instructions that arrive and change by email and phone.

Other jurisdictions are turning the pause before a transfer into public plumbing. California escrow gets no such grid. The DFPI examines after the fact. The FBI's recovery tools engage after the fact. The carrier engages after the fact.

So the pre-transfer moment — the one Singapore decided was worth national infrastructure — exists in escrow at exactly one place: your desk, in the minutes before release. And it is the only moment an examiner, a carrier, or a court will later ask to see.

Intervention as infrastructure

Singapore spent years making scam defense ordinary. ScamShield is a national app, a checking service, and a 24/7 helpline — 1799 — that anyone can call before acting on a request that feels wrong. The premise is blunt: people do not need convincing that fraud exists. They need somewhere to take a doubt in the sixty seconds before they act on it.

The government's annual brief credits the approach with movement. Reported scam cases fell 27.6% in 2025, to 37,308. Losses fell 17.9%, to roughly $913 million.

Two honest notes before borrowing anything. These are national consumer-scam figures, as reported by the agencies that run the programs — nothing in them is about escrow, and a reported-case count moves for reasons besides fewer scams. And the model comes with tradeoffs a US office would never be offered: banks and police sharing customer signals in near real time.

The design insight travels anyway. The only cheap moment in a fraud is before the transfer. Afterward, everything is slow, expensive, and uncertain — a recall is a request, not a command, as our wire recall guide lays out. Singapore built an apparatus around owning the cheap moment.

Nobody is building this for escrow

There is no Anti-Scam Centre watching your trust account. No automated channel between your bank, your title partner, and a police unit that texts your seller mid-fraud.

If one review moment is carrying all the weight, that moment deserves structure. A consistent set of checks. Done the same way on every file. Written down as they happen.

A small office can also borrow the most transferable piece of Singapore's design, and it is not the technology. It is the existence of a place to pause. The helpline works because a person who feels unsure has somewhere specific to take that feeling before acting.

The office version costs nothing. A standing rule: any officer with a doubt about a disbursement brings it to a named second person before release, and doing so is treated as competence, never as slowness. A doubt with somewhere to go becomes a check. A doubt with nowhere to go becomes a wire.

Picture the escrow version of one of those 3,800 alerts. It is not a text from a government system. It is a processor walking a change email over to the officer and saying the bank name does not match the one from the call. That alert only fires if the office made room for it. And it only counts later if someone wrote it down.

The callback is not the problem

I want to be fair to the callback, because this is not an argument against it. Calling a number you already trust to confirm changed instructions remains one of the most useful things an office can do.

The problem is what survives. In most files, the callback lives on only as a memory — "we called, it checked out" — and a memory answers none of the questions that come later. A callback is no longer enough unless the record shows how it was performed. As we wrote when a caller impersonating a bank fraud department talked a California office into 40 wires in one afternoon, the voice on the line is not the control. The documented conduct of the check is.

What should be written down before money moves

Before the money moves, the file should answer five questions:

- What changed.

- What was checked, and against which source.

- What stayed open.

- Who reviewed.

- What the office did.

For a callback, that means the number dialed and its source row — where in the file it came from, and that it was not supplied with the change. The name of the person reached. The facts confirmed, listed. Anything unresolved, retained as an open item. The reviewer and the time. And the office's decision: released, or held pending an owner exception.

Ten lines, written at the moment of review, doing the work a national alert system does elsewhere.

Operator takeaway

You cannot build ScamShield for an office of six. You can build the one moment it exists to reach.

Keep the callback. Stop letting it evaporate.

Singapore made the pause before a transfer into national infrastructure.

In escrow, the pause is yours — and the file is the only place it shows.

— Sebastian Heyneman

Sources

- Anti-Scam Centre and five banks foil over 600 scam attempts (Singapore Police Force, July 7, 2026)

- ScamShield (Singapore government portal), including the 2025 Annual Scams and Cybercrime Brief figures

- Related on this blog: How to Handle a Wire Recall Request After Funds Have Already Disbursed

Boundaries: all figures are as reported by the Singapore Police Force and ScamShield; the dollar amounts are as reported; the Singapore Police release does not specify currency, and given the agency context we have not converted the figure. None of the reporting concerns escrow. The transfer to the escrow desk is our reading, not theirs.

See a sample Review Record.

One page showing what changed, what was checked, what stayed open, and who reviewed it.